")

delihayat/iStock through Getty Photos

Rommel Inc. (NASDAQ:RUM), positioned because the free-speech-focused various to Google’s YouTube (GOOGL), made its public debut in September 2022 through a SPAC merger, with a valuation of $2.6 billion. This appreciation is in stark distinction to its valuation gross sales on the time, which had been lower than $10 million. Rumble’s dedication to selling a free and open web attracts parallels with the mission of Elon Musk’s This media consideration, mixed with robust public opinion, makes Rumble’s inventory notably risky.

Inventory development since September 2022 (SeekingAlpha.com)

It is not simply the corporate’s efficiency that influences its share worth, but in addition public sentiment and the media consideration it receives. On the identical time, it may be mentioned that this media consideration advantages the expansion of the corporate. A current enhance in 81.56% of the share worth adopted Rumble’s announcement collaboration with Barstool Sports activities and its launch new stay streaming software. Nevertheless, for long-term traders it could be untimely to take a place. Regardless of a rise in turnover and the variety of customers, the corporate’s valuation appears excessive.

Rumble’s future success will largely depend upon its insiders’ dedication to long-term progress and never simply opportunistic development waves. That is why I like to recommend a wait-and-see strategy.

Litter overview

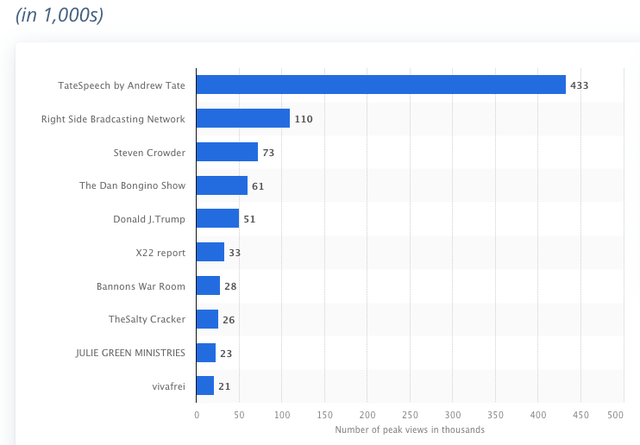

Rumble, a Canadian on-line video platform, website hosting and cloud companies firm based in 2013, has positioned itself as a YouTube rival, providing a platform that’s strongly against censorship. This angle has attracted a major consumer base in a short while, offering vital promoting income and progress alternatives for the creators. The corporate has drawn consideration from a number of the extra polarizing people sharing content material on its platform, comparable to Andrew Tate, Russell Model and former president and present candidate Donald J. Trump.

Standard Content material Creators (Statista.com)

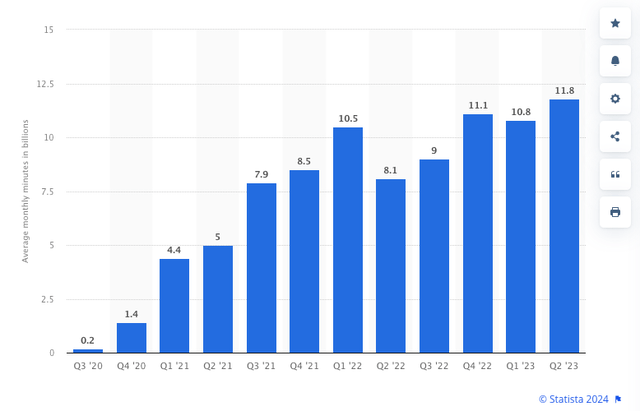

Nevertheless, additionally it is a really engaging house for small and new creators as a result of, not like YouTube, Rumble doesn’t have the brink requirement to start out getting cash. It generates its income primarily by commercials. Extra customers and better engagement imply extra advert views, which results in greater advert income.

Common month-to-month minutes of content material watched on Rumble worldwide (Statista.com)

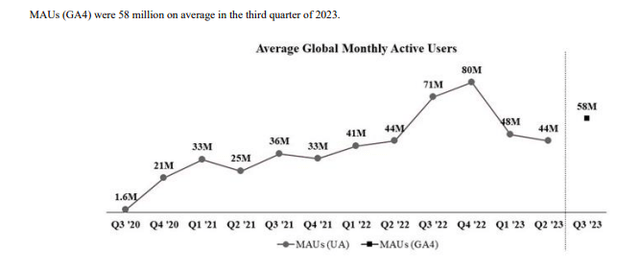

Rumble signifies progress by month-to-month energetic customers (MAUs), that are labeled as anybody viewing the platform from any machine. We might see 76% year-over-year progress to 44 million MAUs in Q2 2022. By This fall 2022, MAUs had been up 142% to 80 million. Nevertheless, within the third quarter of 2023, MAUs fell to 58 million. It is too early to grasp whether or not energetic customers might be frequent guests to the location, and the corporate hasn’t offered any particulars on the expansion within the variety of registered customers.

Month-to-month Common Customers (Sec.gov)

Rumble has entered right into a strategic partnership with Barstool Sports activities to carry unique content material to its customers. This partnership has the potential to draw a broader viewers to Rumble and enhance the platform’s visibility. Moreover, the current launch of Rumble’s livestreaming product is anticipated to extend engagement alternatives and convey monetary advantages to the corporate sooner or later.

Barstool Partnership (Rumble.com) Dwell streaming platform (firm web site)

Messy monetary figures

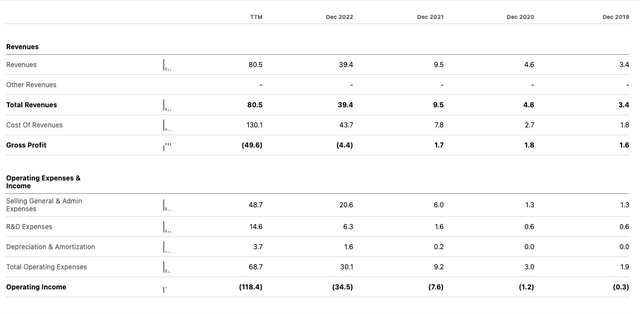

Stepping away from the web buzz and taking a more in-depth have a look at Rumble’s financials, it stays troublesome to justify an preliminary valuation of $2.6 billion. The corporate’s income has proven promising progress, however TTM income is just $80.5 million. Furthermore, rising prices have led to a rise in losses year-on-year. It is price noting that it isn’t unusual for tech corporations, particularly these of their progress levels, to function within the pink. The primary focus right here is on Rumble’s progress and its potential to develop into worthwhile sooner or later. The corporate expects to achieve breakeven in 2025, which could possibly be a turning level for its monetary efficiency. Though the corporate is experiencing money burn, it nonetheless has a wholesome money reserve. This can permit Rumble to proceed investing in its enterprise operations, notably within the anticipated progress of advert monetization.

Annual Gross sales and Working Earnings (SeekingAlpha.com) Annual Internet Earnings (SeekingAlpha.com)

As anticipated, there’s loads of money burn within the progress section of an organization, which we will see within the more and more adverse free money stream.

Delivered Free Money Circulation (SeekingAlpha.com)

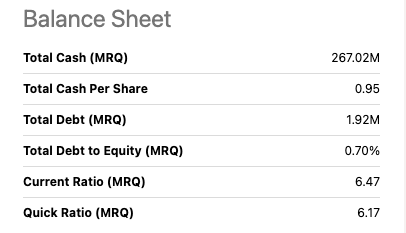

On the stability sheet, Rumble seems to be in a sturdy place. Money and short-term investments symbolize $267.02 million, indicating a wholesome liquidity place. Nevertheless, there’s first rate annualized money burn when in comparison with $338.3 million the 12 months earlier than. The corporate’s whole debt is comparatively low at $1.92 million, which is a optimistic signal. A decrease debt burden reduces monetary threat and provides the corporate extra room to put money into progress alternatives. Quite a lot of the cash goes into the content material acquisition technique. As advert revenues enhance, much less of the money stability will should be spent on creators, which administration estimates will occur by the tip of 2024.

Steadiness sheet overview (SeekingAlpha.com)

RUM inventory valuation

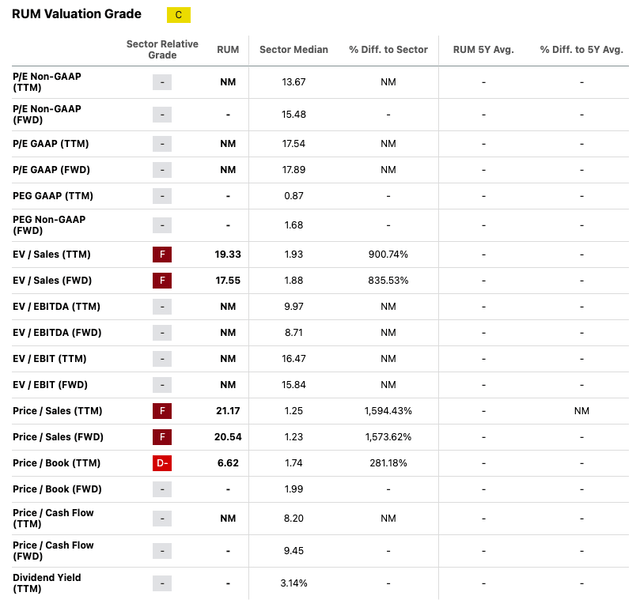

Rumble is a speculative and risky inventory, with a trajectory that’s troublesome to foretell as a consequence of its quick historical past. Regardless of spectacular income progress, the inventory has seen a major decline of 49.04% over the previous 12 months. Nevertheless, the tide appears to be turning for Rumble. Prior to now 5 days, the inventory has risen by as a lot as 81.56%. This uptick is essentially attributed to the announcement of a partnership deal and the launch of its livestreaming product. It is price noting that Rumble’s efficiency can also be influenced by its affiliation with political and polarizing figures. These connections can affect market sentiment, typically independently of the corporate’s precise efficiency. Taking a look at Alpha’s quantitative evaluation, Rumble provides a ranking of “C.” Whereas this is not a high rating, it does not essentially spell doom for the corporate. Rumble’s market cap at present stands at $1.37 billion. That is considerably decrease than the unique valuation of $2.6 billion. Regardless of this decline, the corporate’s valuation stays excessive in comparison with its monetary efficiency. That is mirrored in all valuation ratios, indicating that the inventory could also be overpriced.

Quantitative Valuation (SeekingAlpha.com)

Last ideas

Rumble has been a focus in on-line discussions as a consequence of its positioning as a free speech various to YouTube. Regardless of the commotion, the monetary figures present a much less rosy image. The corporate’s TTM revenues are $80.5 million, a determine that pales compared to its preliminary valuation of $2.6 billion. Prices have escalated, resulting in better losses year-over-year. Nevertheless, this isn’t uncommon for expertise corporations of their progress section. The corporate expects to interrupt even by 2025.

Regardless of the money burn, Rumble Inc. has a wholesome money reserve, permitting continued investments in enterprise actions. The market is extremely reactionary on this inventory, based mostly on information occasions fairly than purely monetary and firm updates, making it a dangerous inventory so early. That is why I like to recommend a wait-and-see strategy for long-term traders.