")

Torsten Asmus

The iShares Funding Grade Company Bond Buywrite Technique ETF (Bats: LQDW) seeks to trace the funding efficiency of an index that displays a method of holding and promoting the iShares iBoxx $ Funding Grade Company Bond ETF (LQD) one month coated name choices to generate earnings. Since coming to market in August 2022, it has truly misplaced cash as losses on its LQD holdings have outweighed the impression of excessive earnings funds. We’re more likely to see a reversal on this efficiency in 2024 as excessive Treasury yields and implied volatility lead to robust earnings, whereas leaving room for vital directional strikes that would see LQDW decline and/or underperform versus of the LQD, has decreased.

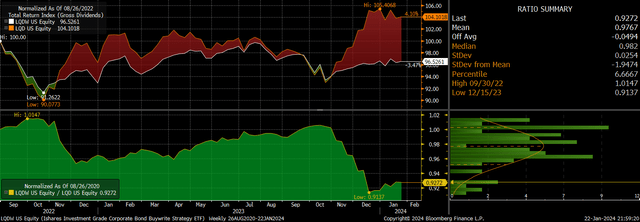

LQDW vs. LQD complete return efficiency (Bloomberg)

The LQDW ETF

The LQDW maintains a portfolio of LQD, which consists of US dollar-denominated funding grade securities company bonds, with a yield to maturity of 5.2% and a mean time period of 13 years. The LQD’s excessive maturity of 8.4 years, mixed with the low default danger, implies that it’s primarily pushed by adjustments in rate of interest expectations. The LQDW then sells for one month on the cash referred to as on the LQD, which permits it to generate excessive earnings, however which means that the fund doesn’t take part within the upside of the LQD. The 0.34% charge pales compared to the return, which presently stands at 19.3%.

The LQDW makes use of the identical technique because the iShares 20+ Yr Treasury Bond BuyWrite Technique ETF (TLTW) and the iShares Excessive Yield Company Bond BuyWrite Technique ETF (HYGW), which additionally use coated calls to generate excessive earnings. The LQDW has a barely decrease return than the TLTW’s 20.3% as a result of latter’s larger volatility ensuing from its longer length. Nevertheless, its yield is larger than HYGW’s 15.9%, regardless of being uncovered to decrease credit score danger.

Falling rate of interest volatility to help LQDW outperformance

If the LQD manages to submit constructive returns for twelve consecutive months, it may be anticipated to generate 19.3% over the following 12 months as a result of mixture of the LQD’s yield and the decision possibility earnings. That is clearly the best-case situation, however even vital losses on the LQD would nonetheless permit the LQDW to earn a constructive return. The LQDW ought to outperform the LQD except we see a big diploma of volatility, which appears unlikely.

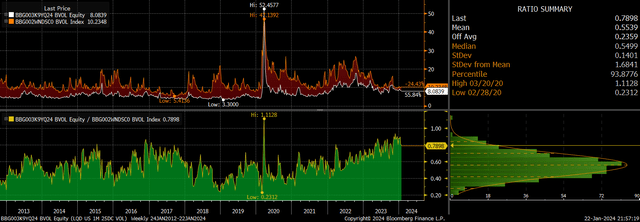

Whereas fairness markets have seen a decline in implied volatility in latest months and years, ranges of implied volatility on the LQD stay excessive. The next chart reveals the volatility of the 1 month 25 delta name choices on the LQD versus the S&P500. The unfold is now near its tightest degree prior to now decade. Provided that the LQD has traditionally been a lot much less risky than the S&P500, this presents a possible alternative.

LQD vs SPX Implied Name Volatility (Bloomberg)

This view is supported by the outlook for US authorities bonds, the place a significant transfer appears unlikely. Upside dangers to Treasury yields seem like restricted by the necessity for the Fed to stop authorities borrowing prices from spiraling uncontrolled. Whereas the Fed’s official mandate is value stability and full employment, its position as lender of final resort to the Treasury Division implies that it stands prepared to stop a pointy enhance in borrowing prices that will in any other case outcome from persistently excessive finances deficits. The Fed’s coverage shift final October in response to the disorderly rise in yields was a transparent indication of this and an identical rise in yields is unlikely to happen once more.

Then again, market expectations for charge cuts this 12 months seem too aggressive, with a 150 foundation level easing priced in over the following twelve months. It will take a major drop in inflation and/or progress earlier than rates of interest might be reduce sufficient to drive down authorities bond yields. Even when this have been to occur, it will possible imply credit score spreads would rise, dampening LQD positive factors and permitting LQDW to outperform.

Renewed inflationary pressures pose the best danger

The largest danger to the LQDW comes from a renewed rise in inflation. Not solely would this put upward strain on company charges on the expense of the LQD, however it might additionally result in a rise in volatility. In contrast to many of the previous decade, LQD volatility has grow to be positively correlated with market-implied long-term inflation charges, and an oil spike, for instance, might trigger an increase in each inflation and volatility.

Resume

The LQDW has struggled over the previous 18 months, with the buywrite technique struggling capital losses throughout final 12 months’s rate of interest spike however failing to take part within the subsequent rally since October. 2024 will possible be a lot kinder to the ETF, as a better yield on its LQD and a extra reasonable outlook for rate of interest volatility will permit it to outperform.